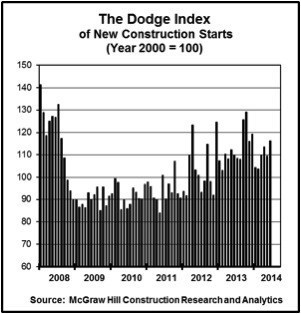

June’s data raised the Dodge Index to 116 (2000=100), up from 109 in May. During the first two months of 2014, the Index had averaged a sluggish 104, but then the pace of construction starts began to pick up, as the  Index averaged 112 over the next four months. “The first half of 2014 revealed a mixed performance by project type,” stated Robert A. Murray, chief economist for McGraw Hill Construction. “Single family housing stands out as the biggest surprise on the negative side, as its upward trend present for much of 2012 and 2013 has stalled for now. Public works and electric utilities are seeing generally decreased activity, as expected. On the positive side, multifamily housing is still proceeding at a healthy clip, and commercial building continues to move hesitantly upward, with office construction this year providing most of the support. Manufacturing-related construction surged in the first half of 2014, boosted by the start of several massive chemical plants and refineries, while the institutional building sector is still trying to make the transition from lengthy decline to modest growth. The year-to-date increase for total construction starts, at a slight 1 percent, reflects the lackluster activity present in January and February. More recent statistics suggest that the expansion for total construction is getting back on track in a moderate, if selective, manner.”

Index averaged 112 over the next four months. “The first half of 2014 revealed a mixed performance by project type,” stated Robert A. Murray, chief economist for McGraw Hill Construction. “Single family housing stands out as the biggest surprise on the negative side, as its upward trend present for much of 2012 and 2013 has stalled for now. Public works and electric utilities are seeing generally decreased activity, as expected. On the positive side, multifamily housing is still proceeding at a healthy clip, and commercial building continues to move hesitantly upward, with office construction this year providing most of the support. Manufacturing-related construction surged in the first half of 2014, boosted by the start of several massive chemical plants and refineries, while the institutional building sector is still trying to make the transition from lengthy decline to modest growth. The year-to-date increase for total construction starts, at a slight 1 percent, reflects the lackluster activity present in January and February. More recent statistics suggest that the expansion for total construction is getting back on track in a moderate, if selective, manner.”

Nonresidential building in June climbed 12 percent to $214.9 billion (annual rate), after slipping 4 percent in May. The increase came as the result of an exceptional volume of manufacturing projects in June, led by the start of a $3.0billion polyethylene plant in Texas. Other large manufacturing projects that were reported as June starts included a $396-million nitrogen plant expansion in Louisiana and a$375-million refinery expansion in Montana. If the volatile manufacturing category is excluded, nonresidential building in June would be down 11 percent after a 22 percent gain in May. The commercial building sector in particular retreated in the latest month, sliding 27 percent after soaring 33 percent in May. Office construction dropped 49 percent in June following a robust May that included $2.3 billion for the office portion of the new Apple Inc. headquarters in Cupertino, California. June still featured the start of several large office projects, such as a $146-million office tower in Chicago, Illinois and a $143-million office tower in Philadelphia, Pennsylvania. Hotel construction also pulled back in June, dropping 25 percent after a strong May, although the latest month did include $92 million for two convention center hotels in Boston, Massachusetts. Stores and warehouses, which were sluggish during much of the first half of 2014, advanced 5 percent and 15 percent respectively in June. The largest store project entered as a June construction start was a $138-million shopping center in Redlands, California.

The institutional side of the nonresidential market improved 3 percent in June. The healthcare facilities category, which generally weakened in early 2014, increased 36 percent in June as the result of groundbreaking for a $900-million hospital campus in San Francisco, California. The amusement category also posted a sharp June gain, soaring 62 percent with the support of a $375-million arena in Las Vegas, Nevada. In contrast, the educational building category in June receded 10 percent, settling back from previous improvement. Even so, the latest month did include the start of several noteworthy public school construction projects, including a $104-million renovation of a high school in Washington, D.C., a $94-million high school in Severna Park, Maryland, and a $68-million middle school in Lynn, Massachusetts. The other institutional categories witnessed decreased activity in June — churches, down 10 percent; transportation terminals, down 38 percent and public buildings, down 56 percent.

During the first six months of 2014, nonresidential building increased 9 percent compared to a year ago. The manufacturing plant category soared 84 percent, reflecting groundbreaking for several very large chemical plants and refineries, such as what took place in June. The commercial categories grew 3 percent year-to-date, with offices construction up 23 percent as its recovery seems to be finally gaining traction. Over the January-June period, the top five office markets ranked by the dollar amount of new construction starts were San Jose, California; New York, New York; Houston, Texas, Washington, D.C. and Boston. Office construction markets ranked six through ten were Chicago, Illinois; Seattle, Washington; San Antonio and Austin, Texas and Omaha, Nebraska. The year-to-date statistics showed a slight gain for hotels, up 1 percent; but declines for warehouses, down 3 percent and stores, down 11 percent. Institutional building in the January-June period was able to edge up 1 percent, providing some evidence that its lengthy decline has reached an end. Most notable was a 6 percent gain for the educational building category, supported especially by an 18 percent increase for K-12 facilities. However, the other major institutional category, healthcare facilities, fell 5 percent year-to-date. The smaller institutional categories showed a varied year-to-date performance — public buildings, up 26 percent; amusement-related work, up 2 percent; churches, down 15 percent and transportation terminals, down 26 percent.

The 1 percent gain for total construction starts at the U.S. level during the first six months of 2014 came from a varied pattern by geography. Growth relative to the same period a year ago was reported in the South Central, up 9 percent and the Northeast, up 5 percent. The South Central’s increase reflected widespread construction strength in Texas, as well as the boost coming from the start of several massive chemical and refinery plants in that region. The increase in the Northeast reflected the brisk pace being reported for new multifamily construction.The West on a year-to-date basis was unchanged from 2013, while weaker activity was reported in the Midwest, down 2 percent and the South Atlantic, down 5 percent.

Join our thriving community of 70,000+ superintendents and trade professionals on LinkedIn!

Join our thriving community of 70,000+ superintendents and trade professionals on LinkedIn! Search our job board for your next opportunity, or post an opening within your company.

Search our job board for your next opportunity, or post an opening within your company. Subscribe to our monthly

Construction Superintendent eNewsletter and stay current.

Subscribe to our monthly

Construction Superintendent eNewsletter and stay current.