WASHINGTON, D.C. – Associated Builders and Contractors forecasts a continued steady economic recovery for the U.S. commercial and industrial construction industries in 2016. Despite a weak global economy, the industry’s solid economic recovery in 2015 should continue in 2016, led by strong consumer spending.

WASHINGTON, D.C. – Associated Builders and Contractors forecasts a continued steady economic recovery for the U.S. commercial and industrial construction industries in 2016. Despite a weak global economy, the industry’s solid economic recovery in 2015 should continue in 2016, led by strong consumer spending.

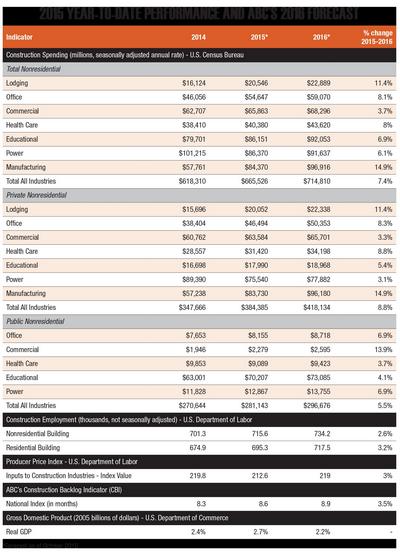

“As the mid-phase of the economic recovery continues, ABC forecasts growth in nonresidential construction spending of 7.4 percent along with growth in employment and backlog,” said ABC Chief Economist Anirban Basu. “The mid-phase of the recovery is typically the lengthiest part and ultimately gives way to the late phase, when the economy overheats. The current recovery could end up challenging the lengthiest recovery in U.S. history, which lasted 120 months between March 1991 and March 2001.

“Already, signs of overheating are evident, particularly with respect to emerging skills shortages in key industry categories such as trucking and construction,” said Basu. “Despite that, average hourly earnings nationwide across all industries collectively are up only 2 percent in the past year, well below the Federal Reserve’s goal of 3.5 percent. There are also indications that certain real estate and technology segments have become overheated, with purchase prices rocketing higher and capitalization rates remaining unusually low.

“ABC’s leading indices each suggest that 2016 will be another solid year for the typical U.S. nonresidential construction firm,” said Basu. “ABC’s Construction Confidence Index encompasses expectations with respect to hiring, profit margins and projected sales growth. According to the most recent survey, overall contractor confidence has increased with respect to both sales (67.3 to 69.4) and profit margins (61 to 62.9). And while the pace of hiring is not expected to increase rapidly during the next six months, largely because of the lack of suitably trained skilled personnel, the rate of new hires will continue at a steady pace. ABC’s Construction Backlog Indicator also signals strong demand during the months ahead. According to the latest backlog survey, average contractor backlog stood at 8.5 months by mid-year 2015, with backlog surging in the western United States and the heavy industrial category.

“A weak global economy and stronger U.S. dollar will prevent the U.S. economy from surging ahead in 2016,” said Basu. “Stakeholders can expect a 2.2 percent rate of growth (or similar to that) next year. There are significant risks to the downside, including volatile financial asset prices. The recent softening of job growth may keep the Federal Reserve pinned on the sidelines for the balance of 2015. Under most conceivable scenarios, rate increases will be gradual and intermittent. However, construction stakeholders can find reasons for encouragement. The U.S. unemployment rate has fallen, and the nation is roughly a year away from full employment. Wage growth is set to accelerate, which should keep the consumer spending-led recovery in place.”

Join our thriving community of 70,000+ superintendents and trade professionals on LinkedIn!

Join our thriving community of 70,000+ superintendents and trade professionals on LinkedIn! Search our job board for your next opportunity, or post an opening within your company.

Search our job board for your next opportunity, or post an opening within your company. Subscribe to our monthly

Construction Superintendent eNewsletter and stay current.

Subscribe to our monthly

Construction Superintendent eNewsletter and stay current.